Designing on-chain Options

The next leg up to billion dollar flows

Introduction to Options

Derivatives are one of the most popular financial tools to hedge and speculate in TradFi markets, estimated to be worth trillions of Dollars. 2022 remained a busy year for options as retail traders and institutional investors tried to hedge the whiplash of the Fed’s rate hikes. Options are leveraged instruments that can magnify investment gains without worrying about liquidation, making them very attractive to retail traders. The daily notional value of traded stock options even crossed average stock trading in the US in 2021 with the proliferation of retail trading apps focusing on simplifying the trading experience.

When it comes to crypto markets, derivatives are estimated to make up a staggering 60-70% of all trading on centralised exchanges worth around $3 Trillion. The most popular type of derivative is the Perpetual Future, a simple trade that involves betting on the price direction of an asset. In contrast, options pricing is affected by multiple factors, including the current price of the underlying asset, the strike price, the expiration date, and the level of volatility in the market.

Deribit, the world’s largest crypto derivatives exchange, controls about 90% of options trading volume and saw its daily options volume peak to $3 Bn in March of this year. While DEXs such as Uniswap succeeded in pulling spot trading volume away from CEXs, decentralized derivatives protocols are still in the works. Option traders have three primary considerations - market-driven pricing, high-capital efficiency, and deep liquidity. As long as decentralized protocols cannot fulfill these demands effectively, centralised protocols will play the lead, and DeFi options protocols will have to play catch-up.

If we look at the historical activity of Bitcoin and Ethereum options, we can observe that Bitcoin options are traded more frequently, with volumes nearly twice that of Ethereum. In 2021, the monthly volume of Bitcoin options peaked at $30 billion, but currently, it stabilises around $20 billion, barring the unusual spike in March 2023. This extraordinary volume increase was likely due to the banking crisis coupled with Balaji's bold prediction in March that Bitcoin would hit $1 million within a 90-day timeframe. Options provided a convenient avenue for traders to participate in this speculation with limited downside risk. Bitcoin options can only be purchased via centralized platforms that mirror traditional finance options. In contrast, Ethereum, Solana, and Layer 2s are persistently laying the groundwork for non-custodial options using smart contracts.

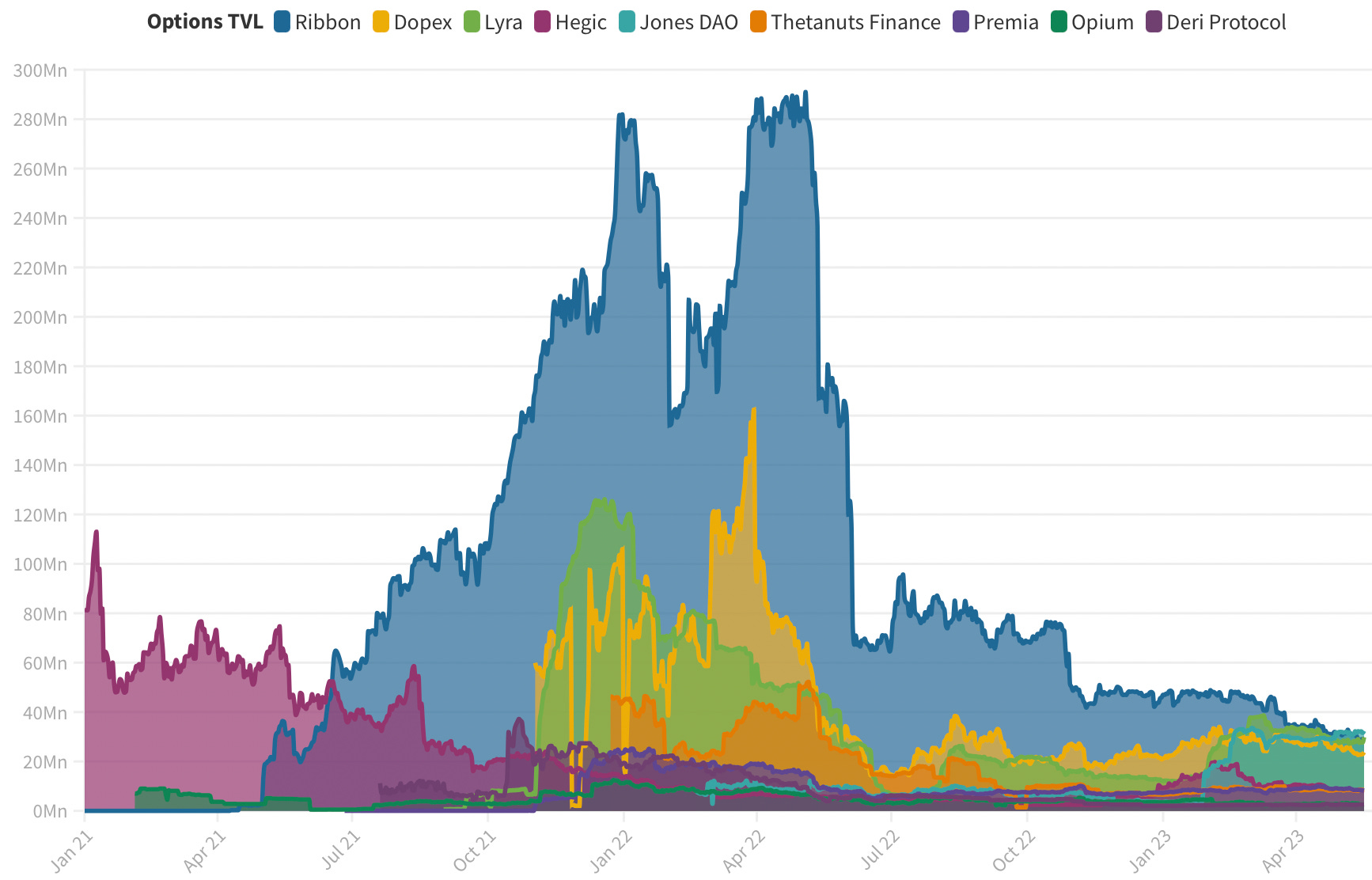

During the DeFi boom of 2021, options saw significant growth, particularly with Hegic, an on-chain peer-to-pool based exchange that managed to attract $100 million in Total Value Locked (TVL). Ribbon Finance innovated with Decentralized Option Vaults (DOVs), designed to generate yield through option underwriting. These DOVs used liquidity providers' capital to earn yield and sold these options to professional market makers with the best bids, allowing them to price these options and effectively hedge the risks associated with holding these options until maturity.

The landscape shifted as Automated Market Maker (AMM) Option protocols like Lyra and Dopex began selling options not just to market makers, but also to retail traders. Both Lyra and Dopex, which were launched at the end of 2021, grew rapidly to reach a TVL of $100 million. However, as the markets began to struggle in May of the previous year, all protocols experienced considerable drawdowns. This may be due in part to high market volatility deterring option writers who struggled to effectively hedge these risks.

Currently, Ribbon Finance is the only Ethereum protocol with a TVL exceeding $25 million, even though its TVL plummeted by as much as 90% from its $300 million mark on April 22nd. Both Jones DAO and Lyra have made strides to migrate to new Layer 2 solutions in an effort to reduce transaction costs and broaden their user base.

The Complexity of Pricing Options

Option pricing models are trying to bring structure to an unpredictable future. Derivatives are second-order effects of the underlying stock and hence they move at accelerated rates. To keep track of this, market makers use complex pricing strategies running on expensive infrastructure. This problem space is one of the most lucrative and infamous fields in mathematics and economics. Black-Scholes, the most used equation to price options was awarded the Nobel prize in 1968. However BS model comes with a lot of assumptions, one of them being that the price follows a geometric Brownian motion with constant volatility. The BS model is therefore applied by employing "implied volatilities", volatilities that are backed out from other market prices for different maturities and strike prices. BS models take into account five variables to calculate the price of an option: the underlying asset's price, the strike price, the time until expiration, the risk-free interest rate, and the implied volatility of the underlying asset.

Crypto markets are risk-on assets and more volatile than traditional markets. That’s why they are prone to big swings, like the January bear rally when markets shot up by 50% while everyone was expecting prices to go lower. Because they are prone to big swings, one can implicitly understand that there is a higher chance of high price fluctuations and options being very rewarding when the markets go in your favor.

Implied volatility is the most important component of the model because it reflects the market's expectation of the underlying asset's price movement and volatility. Higher implied volatility implies that the market expects the underlying asset's price to be more volatile, which increases the price of the option.

Traders want deeper markets and tighter spreads. This requires market makers who can manage risk effectively even during black swan events. TradFi exchanges use the CLOB(Centralised Limit Order Book) model to settle orders. This means that you place an order and wait for someone to fill it. There is a counterparty that has to take the opposite position. If the market is not deep, there won’t be a counterparty to fill your order and you will need to pay higher prices. Decentralized option protocols offer several advantages over traditional options: Trustlessness - Removes the risk of counterparty default or order manipulation by exchange, Accessibility - Available to anyone without intermediaries, Liquidity- AMMs can provide continuous pricing even in low volume markets, Flexibility - Enables traders to customize their self-custodial positions and implement complex trading strategies.

The difficulty with replicating options through decentralized protocols is twofold - order matching, and clearing house risk. In TradFi, the exchange acts as a central authority that can understand the flexibility of option payoffs and match counterparties. Once the orders are matched, the clearing house becomes the central counterparty- the buyer to every seller’s clearing member and the seller to every buyer’s clearing member. The clearinghouse evaluates the margin collateral for every order, monitors positions continuously, settles margins on a daily basis and has a recovery plan in case any party defaults. If one party is unable or unwilling to fulfill their obligations, the clearing house can take legal action to enforce the contract.

In the case of decentralized derivatives, there is no central party that acts as a clearing house. If a party writes an Ethereum call option for $1000 and the price of Eth reaches $2000 at the time of settlement, the writer has to bear the loss of $1000. If this was an under-collateralized option and he only deposited 10% or $100 as margin, there is no incentive to settle this option and pay the balance of $900. This is why options sellers are sophisticated investors who hedge their positions to eliminate the risk of default.

In essence, decentralized derivative protocols are trying to wrestle with volatility and time to minimize the losses to both option buyers and writers, match counterparties efficiently, and find the optimum price at which traders can hedge their positions.

There are different types of option structures, the most common ones being American options and European options. BS model cannot be used to price American options because it assumes that the option can only be exercised on the expiration date. The most common method for pricing American options in TradFi is the lattice model which incorporates a range of possible outcomes and requires continuous scrutiny.

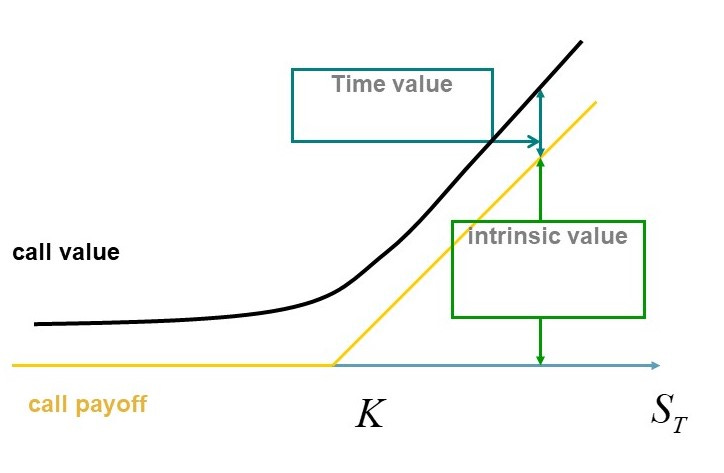

For options, we have to distinguish between selling the option and exercising the option. Exercising the option means we get the payoff max(0,S-K) for call or max(0, K-S) for put. We can sell both European and American options at any time (as long as we have a buyer), however, we can exercise American options but not European options prior to maturity. For ex- if you bought an option that expires 6 months away and the current stock price is below the strike price, the call option would not be worthless because it has time value but exercising the option would be worthless. As American options can be exercised at any point in time, they have higher optionality and hence command higher premiums.

Deribit offers European options which means that you cannot exercise the option before expiry. If you want to profit from your position at any time, you can sell off the option to a third party provided you are able to get an interested buyer. DeFi protocols have favored the utilization of European options due to their payoff structures being readily codifiable within smart contracts. Most DeFi protocols use BS models to price options. New pieces of infrastructure such as Panoptic are trying to move past the BS model and create payoffs utilizing Uniswap’s liquidity infrastructure.

Defi Options Landscape

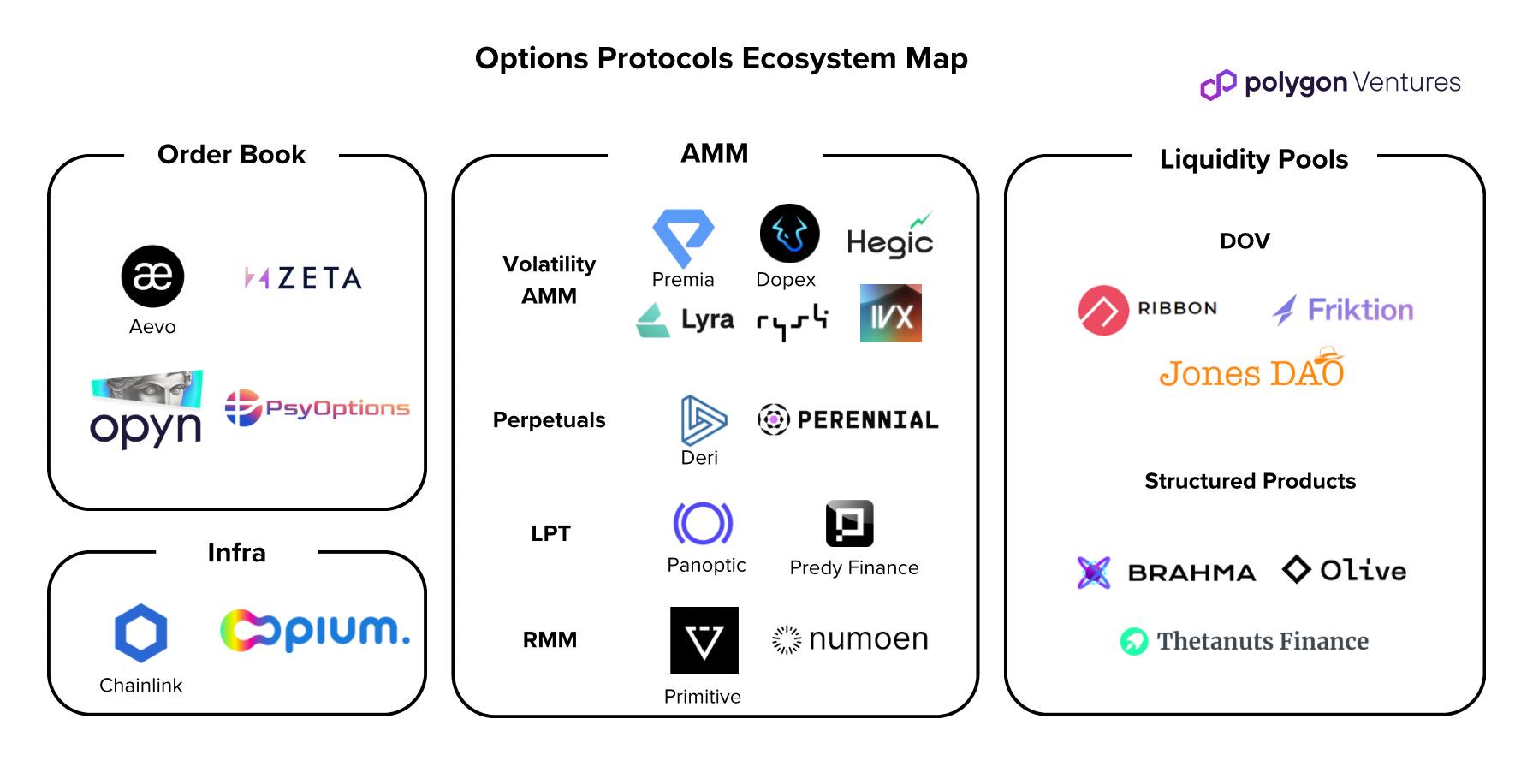

Teams working on decentralized derivatives must evaluate the tradeoffs of managing clearing house risk and match orders with high capital efficiency. We can broadly classify the DeFi options landscape into four segments: Order book, Liquidity pools, AMMs, and infrastructure providers.

Orderbook DEXs operate in a peer-to-peer model where the exchange has to find counterparties willing to match the trade.

Automated Market Maker (AMM) models operate in a peer-to-pool model and facilitate trading by pooling liquidity. However, DEX AMM models that are effective for spot assets may not be suitable for options, as Options require the ability to express preferences for future time horizons. Additionally, it is worth noting that the top 10 Option protocols by Total Value Locked (TVL) are peer-to-pool models, highlighting the crucial role of liquidity as a network effect for financial applications.

Decentralized option vaults are quite popular, as they allow users to earn a yield on their deposited funds by writing options and collecting premiums. These funds are securely locked into a smart contract with predefined expiration terms. While some liquidity pools rely on off-chain market makers to buy these options, others feature integrated AMMs, which leverage the pool's liquidity to price options for any trader to buy. Structured products expand the functionality of DOVs to create complex strategies such as principal-protected vaults.

Lastly, infrastructure protocols provide the necessary tools, systems, and support to facilitate the smooth functioning of options trading on decentralized platforms. These providers play a vital role in creating and maintaining the infrastructure required for decentralized options trading, which includes pricing feeds, liquidity management, auction-based settlement, handling liquidations, and other technical capabilities.

Order books

Order book powered DEXs try to match buyers and sellers based on their trading needs and settle trades on chain. CLOB-based DEXs rely on a transparent real-time list of buy and sell orders, to match trades. Orders are executed based on price and time priority, ensuring a fair and orderly market.

High-performance chains like Solana and NEAR have allowed for the creation of on-chain order books with low latency and cheap transaction costs. Zeta leverages Solana’s 400ms block time to update prices and monitor positions multiple times per second, enabling the implementation of an under-collateralized trading experience.

Layer 2 solutions are feeling more innovation with teams working on high-performance rollups that can match trader’s expectations. The Ribbon finance team is building Aevo, a custom EVM rollup that handles order matching off-chain and settles on-chain. Aevo's risk-matching engine evaluates collateral before order placement, enabling collateralized options. We expect more breakthroughs in this area through new rollups and collaboration with risk management engines to bring order matching on-chain.

Aevo’s OTC and Synquote are building RFQ-based order matching protocols which operate slightly differently. Dealers provide off-chain quotes based on a buyer's or seller's request, and the requester then selects the most appealing quote. While this lacks the immediacy of CLOB, it provides traders with the opportunity to 'shop around' for the best deal when executing large transactions.

Liquidity Pools

DOV:

Ribbon Finance pioneered Decentralised Option Vaults(DOV) to generate returns for passive assets by underwriting call options and capturing the yield. They have played a significant part in the ‘Real Yield’ narrative as they generate income from external parties rather than token-designed incentives that extract value out of the protocol in return for propping up liquidity.

DOVs wrap the option underwriting process into an accessible format so that retail users can profit off option strategies without the complexity of calculating premiums, strike prices, volatility, and suitable dates to buy calls and sells.

Investors deposit their assets in DOVs and lock them up for a specified period, as determined by the vault's conditions. These vaults typically offer options that expire within a one-week time frame. By pooling all users' assets as collateral, the vault calculates the strike price for options that expire the following week using proprietary algorithms to minimize writers' losses. These newly minted options are then sold to off-chain market makers through a blind auction process, with the highest bid receiving the option tokens. At the time of expiry, if the options are out-of-the-money (OTM), the option tokens expire worthless, and the collateral is returned to investors. If the options are in-the-money (ITM), the vault settles the profit from the collateral and returns the remaining funds to investors.

Vaults are fully collateralized - As there is no central authority to enforce delivery of assets, DOVs lock in assets from the time of purchase until settlement and typically only offer covered calls or protective puts. The most common strategies sold are covered calls and protective puts where the underlying is collateralized. This helps to ensure that the full exercise value of an option can be paid out to option holders in the event that the option is exercised. However, because vaults require full collateralization, they have less capital efficiency and cannot support anytime entry/exit liquidity.

Vaults cannot express long term options- DOVs typically sell only weekly calls because weekly returns follow a normal distribution and users don’t want to lock their assets for a long duration. DOVs make it simple for users to earn 15-20% APY when markets are not highly volatile. While these strategies may minimize risk, DOVs are still dependent on market conditions and will take huge drawdowns occasionally.

Vaults pool liquidity together - The existence of many different options expiration dates leads to one additional problem: liquidity fragmentation. If market makers must make markets on options expiring not just this week but every week for the next three months, they will be forced to spread out their capital, making it harder for other participants to execute large trades or to determine fair prices. Vaults increase capital efficiency by reusing the same collateral for options with different expiry.

Vaults combine offchain calculation with onchain settlement- The calculations involving options models are computationally heavy and expressing them on chain is very expensive due to the high gas fees. Vaults typically sell these options to market makers such as Paradigm and QCP Capital who can hedge their risks off-chain. Collateral management, price discovery, and settlement occur on the blockchain using a system of keepers ensuring that the whole process is fully transparent.

DOV protocols have small design changes depending on the protocol construction and blockchain. Ribbon uses Gnosis safe for on-chain auctions while Friktion uses Gradual Dutch Auctions supported by Solana’s RFQ infrastructure. By auctioning off options to the highest bidder, DOVs are offloading the price discovery to market makers and are just focused on simplifying the experience for retail traders to earn premiums.

Vaults face two main challenges:

- The yield that can be earned from the vault is limited by the efficiency of the process used to match buyers and sellers of options contracts.

- They rely on oracles for liquidation, which can create potential vulnerabilities in the system as oracles can be vulnerable to hacking or manipulation.

Market makers and traders who want to hedge long-term positions have to roll their positions when their positions are expiring. To roll options, they have to close options by taking profit and buy options with the new expiration date. Sometimes, this is inefficient as traders will need to enter new positions and pay higher premiums to stay hedged.

Structured Products:

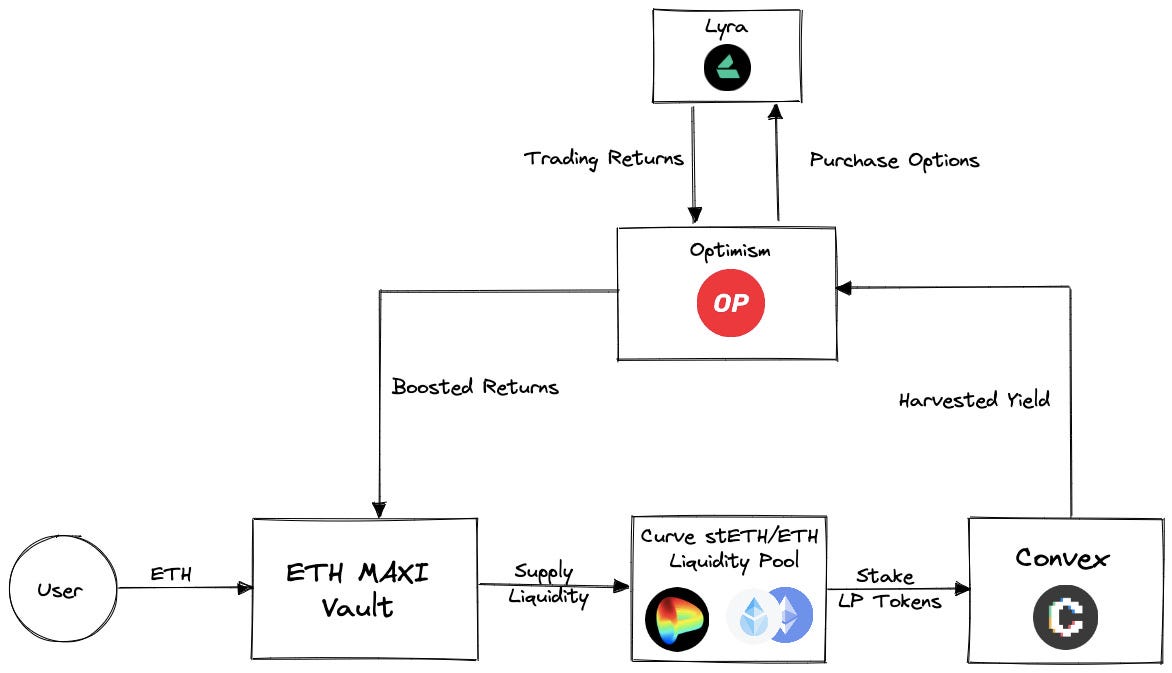

Structured products employ more sophisticated strategies than just covered calls and short puts and are designed to facilitate highly customized risk-return objectives. For example, Brahma’s ETH Maxi vault pools capital from investors and supplies capital to the highest-yielding Curve pool. At the end of every week, all harvested yield is used to take a leveraged bet using a momentum trading strategy. Brahma’s vault buys 1-week at-the-money ETH options (calls if the signal is bullish, puts if the signal is bearish) on Lyra Finance. Using this design, Brahma is boosting its returns by writing option premiums. If the options purchased don’t yield any returns, the premium paid is lost while the principal is protected.

AMMs

Automated Market Makers (AMMs) are decentralized exchanges that enable users to trade directly with automated bots, bypassing the need for peer-to-peer trading. AMMs such as Uniswap, Balancer, and Curve, employ Constant Function Market Maker(CFMM) trading functions to facilitate token exchanges.

With AMMs, the counterparty is an impartial algorithm that fills your order. Bigger the AMM’s pool, the bigger volumes you can transact in and out without slippage. AMMs do not require oracles to monitor external prices, thereby eliminating oracle risk and the need for a system of keepers to track off-chain events, both of which could potentially expose the system to malicious attacks. Instead, AMMs rely on arbitrageurs to rebalance the pool’s portfolio according to the equation x*y=k. Liquidity providers(LPs) supply tokens to earn fees, and traders can swap between tokens with high capital efficiency. This is not to say that LPing in Uniswap is passive income, however, supplying liquidity is less challenging than competing with TradFi market makers.

DEX AMMs cannot input variables of volatility and time which are needed to express option payoffs. Moreover, options are complex and leveraged products with significant risks. This is why existing oracle-less AMM designs cannot be directly applied to options trading. Option AMMs must resort to using oracles to source volatility data and the funding rate from external markets to accurately calculate premiums. LPTs and RMM’s are new infrastructures that are working on oracle-less options which we will dig into below.

Additionally, it is worth noting that options AMMs are less expressive than DEX AMMs, with only Premia and Perennial allowing the selling of options back to the pool. Most AMMs only support European options, where users cannot exercise the option until expiry with Premia being the exception. Most AMMs are not capital efficient: only a few including Lyra, Premia, Perennial, and Panoptic support under-collateralization.

Volatility based AMMs

Volatility-based AMMs create liquidity pools from LPs who are interested in earning premiums through underwriting. LPs lock capital into vaults and the AMM writes covered calls and protected puts similar to DOVs. These options are then priced by the AMM and sold to investors in return for a premium.

As we discussed above, pricing options is tricky because they require adjustments according to contract term structure, market beliefs, liquidity depth, availability of market makers, and Implied Volatility.

Volatility AMMs observe prices on CEXs and calculate implied volatility using proprietary methods which are then used as the input to compute option prices for different strikes and expiries. Implied volatility is very subjective without liquid order books and deep markets. Hence Volatility AMMs cannot address long-tail options. If options are mispriced, traders can seize these opportunities and LPs lose the capital that they locked into the vault without being compensated with sufficiently high premiums. Buying options back into the pool requires extensive risk management because AMMs that purchase mispriced options can accumulate bad debt. LPs who frequently take drawdowns lose interest in the protocols and stop supplying liquidity, harming the market.

Premia plots a 3d plot of the volatility of the option off-chain and uses Chainlink to bring this Volatility Surface on-chain. Premia uses this input along with the pool utilization rate to accurately price options and ensure maximum capital utilization and higher returns for LPs. Dopex adjusts Implied Volatility through a decentralized consensus between trusted crypto market makers who vote on the steepness of the IV curve.

Lyra’s protocol aims to hedge overall protocol risk to provide deep liquidity and price options competitively. While Delta is a big topic that we won’t go into here, it essentially describes the risk associated with changes in the price of the underlying asset. Lyra sums up delta risk for every option in its basket and prices options such that the AMM be close to delta-neutral, smoothing the exposure of the AMM to a large directional move in the underlying and reducing PNL fluctuations for LPs.

Rysk operates largely in the same way and prices its options in such a way as to incentivise the sale/purchase of options that bring the DHV's delta exposure closer to zero. For example, suppose the demand for calls outstrips that for puts. In that case, the vault will automatically increase the price of calls and reduce the price for puts, incentivising a market-driven rebalancing of the book's delta. IVX is a new team building an Options AMM on Arbitrum. They plan to hedge the delta exposure by taking a futures position on GMX and periodically adjusting it to stay delta zero.

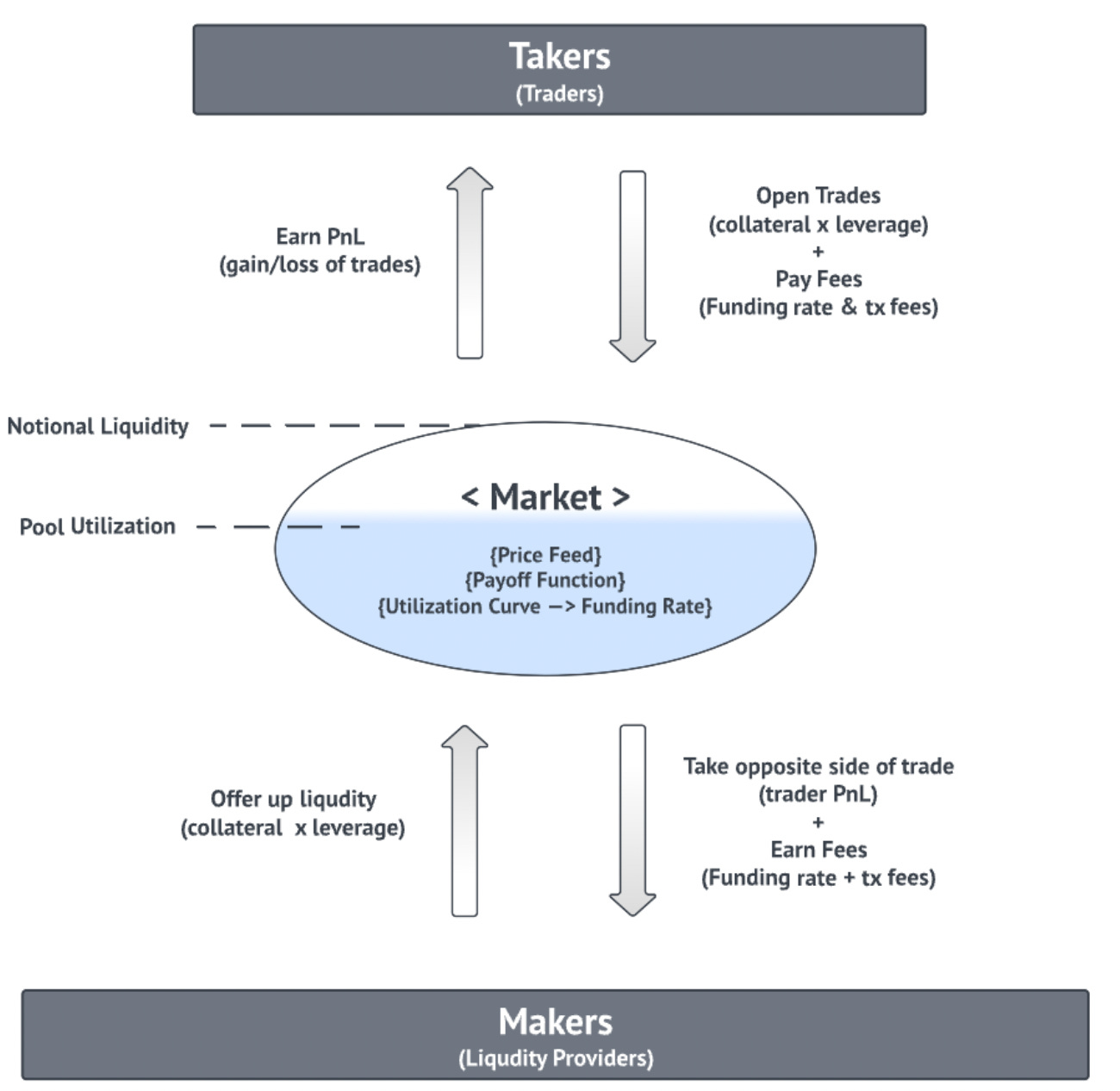

Funding-rate AMM

Everlasting options are a special case of funding-fee-based perpetual derivatives requiring traders to pay a funding fee to take a position and stay hedged. Everlasting Options were introduced by Paradigm and work akin to perpetual futures - those who are long the perp (have bought it) must pay a funding fee to those who are short the perp (have sold it) every day.

Deri is a decentralized everlasting options protocol that launched in Feb 2021. It uses an oracle to get spot price and volatility to calculate the premium that traders need to pay to enter a position. Once a trader decides to open a position, he pays an upfront premium for seven days using the funding rate that floats based on the utilization of the liquidity pool. LP’s supply liquidity and play the role of counterparty for traders. If traders win, LPs lose, and if traders lose LPs win. Positions are maintained daily by settling the funding fees of [Max(UnderlyingPrice - Strike, 0) for call options & Max(Strike - Underlying, 0) for put options]. On a continuous, ongoing basis, LPs and traders settle up; the losing side of the trade pays the winning side.

Perennial is a new funding rate AMM that’s very similar to Deri; with some design changes to allow market makers to customize their risk and take upto 50x leverage. They currently support only perpetual futures and are working on supporting options.

Funding rate AMMs use the BS model to price options, but they simplify trading experience and maximize capital efficiency by encapsulating payoff within the funding fee model. LPs are incentivized to park capital in the pool to reap funding fees and sustain pool liquidity utilization near the 80% threshold. Funding rate AMMs are under-collateralized, allowing traders to enter options positions without depositing collateral and liquidating positions when the loss exceeds margin.

Perpetual futures markets have been on a tear with the likes of GMX and dYdX processing $100Bn+ volume. While perps pool liquidity, options fracture the volume into pools depending on the strike price - ETH1500C, ETH 1800C, ETH2000C, ETH1500P, ETH 1800P. Each of these pools has different premiums and funding fees, making it difficult to replicate the success of perps which are simple up/down trades with leverage.

LPT AMM

Panoptic represents a new approach to options trading, circumventing the traditional clearing house in favour of LP positions within Uniswap v3. Guillaume Lambert, the visionary behind Panoptic, recognized that LPing into Uniswap v3 produces a payoff equivalent to that of a put option.

Panoptic recreates perpetual options payoffs of covered call and cash secured put utilizing Uniswap v3 positions and eschewing reliance on Black-Scholes logic. These LP positions are tokenized as Liquidity Provider Tokens (LPTs), which are then deposited into a Panoptic pool, allowing option sellers to write undercollateralized options with a collateralization ratio at just 20% of the notional value.

Despite not having entered the derivatives market, Uniswap Labs is closely monitoring this evolution and has, in fact, made a strategic investment in Panoptic. The creation of oracle-less, custodial primitives, complemented by the instant pricing and flexible liquidity of automated market makers, represents a significant turning point in the pursuit of leveraged products for any token. Panoptic is still under development and is expected to launch in Q2. If you want to delve deeper into Uni options, check out this low-math explainer.

Other teams such as Predy are also exploring the possibilities of Uni LPTs to develop innovative financial products. Gammaswap and Smilee, for example, are leveraging Uni LP positions to construct volatility products that can help traders bet on a rise in volatility and benefit from large market moves. These endeavours hold great potential for reproducing the complex payoffs that institutions are accustomed to.

RMM

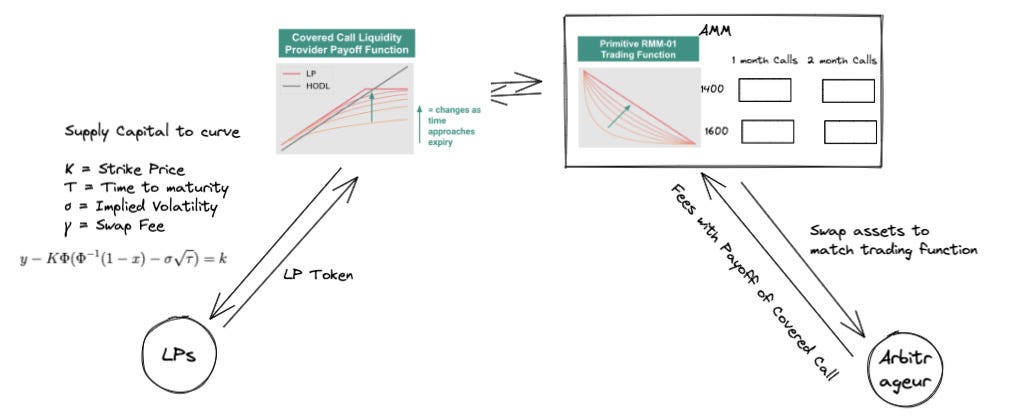

RMMs use algorithms to replicate payoffs of options valuing assets based on price, volatility, and time. RMMs(Replicating Market Makers) have the advantage that you don’t need a direct counterparty and are not dependent on an oracle.

The Primitive team is working on a trading function that replicates a covered call. While Uniswap’s function x*y=k has only two inputs, Primitive’s trading function has multiple inputs that compute the payoff of a covered call. After LPs decide on the strike price and volatility, they supply risky assets (e.g. ETH) and stable assets (e.g. USDC) in the ratio that satisfies the Covered call LP function.

If you want to take a call option on Eth, you need to supply Eth and USDC in the ratios that fulfil the trading function.

For example, if the price of ETH is 1500 USDC, but you believe that one month from now that price will be 1600 USDC, you can express that view by providing liquidity to an RMM that expires in one month (τ = 1 month) with a strike price of 1600 USDC/ETH (K = 1500 USDC). This position has the highest expected return if the price of ETH reaches a terminal value of 1600 USDC at expiry. The caveat is that if you're incorrect about the price path, for example, if ETH goes to 1200 USDC in that same time span, you will lose more through impermanent loss than if you have held ETH.

When liquidity providers add funds to the curve, they receive tokens known as liquidity provider tokens that represent their positions. As the value of the underlying tokens fluctuates relative to external markets, arbitragers trade these tokens and pay fees that accumulate in the LP tokens over the life of the option. Through this process, the pools tend to converge toward the payoff of the covered call. LPs can redeem these tokens at any time by withdrawing their liquidity and receiving the accumulated fees. Primitive's options have some key advantages over vault-based options, such as not requiring oracles and allowing for greater capital efficiency as LPTs can be used as collateral in other protocols.

Options are awaiting their Perpetual moment

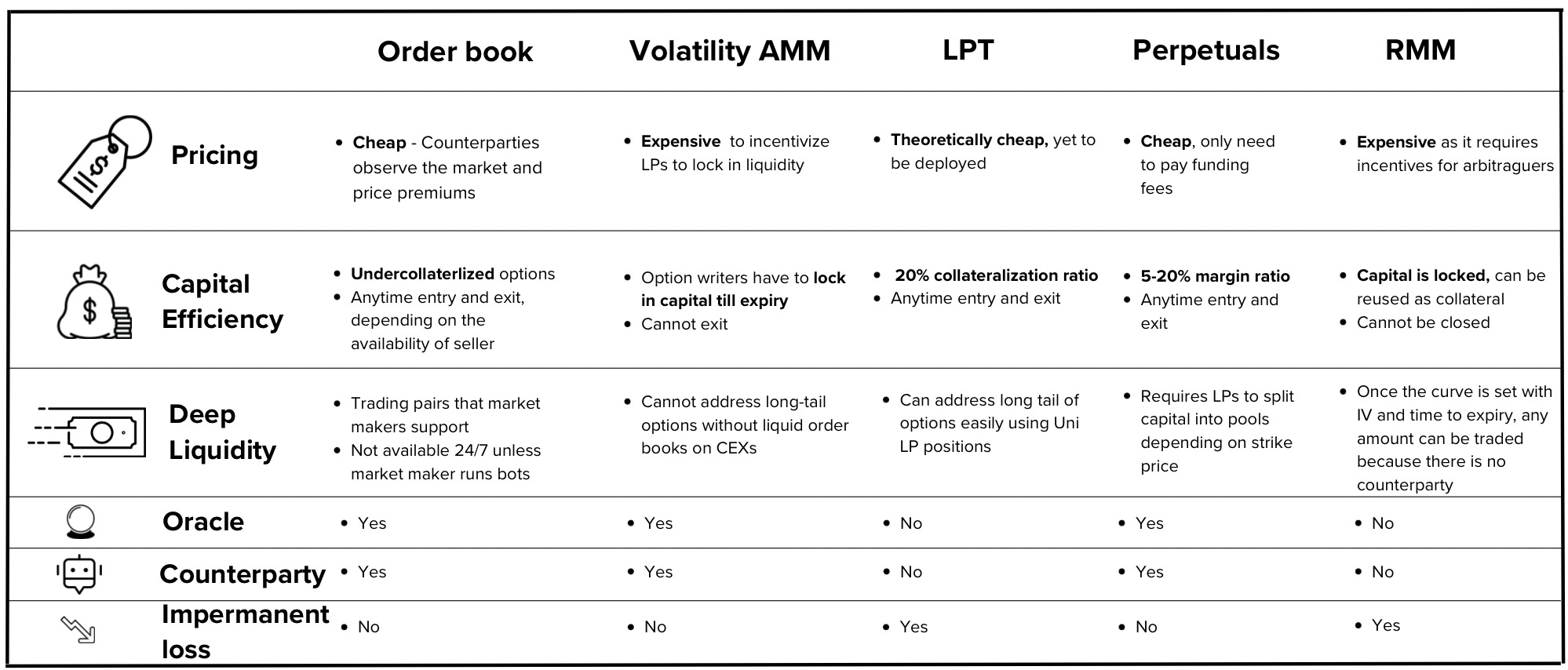

Let’s recap the different designs using the metrics that we highlighted: Pricing, Capital efficiency, and Liquidity.

The path towards decentralizing options has had its fair share of challenges and difficulties such as the inability of LPs to exit at the time of their choosing. The gas costs on the Ethereum network pose a significant barrier to entry. To address this challenge, many DeFi platforms are turning to layer-two scaling solutions such as Arbitrum, Polygon, Optimism, and Starknet. These alternatives offer significantly lower transaction fees, thereby enabling a more accessible and cost-effective user experience. The continuous efforts by DeFi teams have led to the emergence of new and innovative designs, algorithms, and infrastructure. For example, Psyoptions is experimenting with airdropping option warrants rather than tokens, which incentivizes long-term holding and avoids the immediate dumping of tokens. There are some significant improvements that are crucial to onboard retail and institutions:

- Simplified User Experience - Teams are working on breaking down options into actual user needs - Bumper is working on hedging your portfolio by paying an ‘insurance premium’ while using options in the background. Premia provides more insights to speculators to compare the market price of an option with the theoretical option price and provides users with valuable insights into the relative cheapness or expensiveness of an option. This enables traders to make more informed decisions by providing them with a deeper understanding of the market conditions and helping them to identify potential opportunities for profit. Teams are also integrating with bridges to deliver a multi-chain experience where traders can use their assets on one chain to buy options on assets belonging to another chain.

- Oracle-less pricing - If trading relies on off-chain computation, then the advantage of a trustless party is gone. We reached out to Basile who’s the founder of Desma8, a research org focusing on Defi derivatives to understand what’s missing for institutional adoption. According to Basile, there should be a classic European option product with sound pricing that is fully decentralized and has proper risk management (e.g., counterparty default/AMM Market risk). Except for covered call options and order-book approaches, there is no protocol I am aware of, that provides this "classic product"

- Better Risk Management - Each of the protocols surveyed has some shortcomings. For example, if implied volatilities are sourced via oracle then these implied volatilities do not typically reflect the market risk of the AMM and could incentivize trades that further increase the AMM risk. Panoptic has a good approach because the optionality is built in the Uni V3-type mechanism, but they have a somewhat rough approximation to calculate their backward-looking premium and the pricing could be totally off.

- Higher capital efficiency - Perps models such as GMX have been able to condense liquidity into a single pool to enable 50x leveraged trading. With options, each strike price and time to expiry requires a different pool which is 100% collateralized and locked until expiry. Undercollateralized protocols such. as Panoptic and Synquote will free up this capital and enable market makers to supply deeper liquidity.

DeFi options offer new financial infrastructure that goes beyond replicating traditional markets, instead creating entirely new building blocks with the potential to leapfrog tradfi products. If you are building in this space or exploring new designs, we would love to hear from you.

Many thanks to Basile Maire for his thoughtful insights, go give the chad a follow. Shoutout to Nathan, Sanket, & Asif for their feedback.