Horseshoe Wallet Theory

Why web3 wallets are becoming platforms

PayPal's recent partnership with MetaMask to facilitate cryptocurrency purchases may seem like an unlikely pairing, but it actually makes sense for both parties. But why the love between web2’s biggest wallet and web3’s biggest?

TLDR;

- Paypal wants to expand into new markets

- Payment apps derive network effects from their two-sided marketplace of users<>merchants

- Web3 wallets allow users to securely store and send crypto. They don’t have network effects, and they are akin to banks where economies of scale and brand matter.

- Web3 wallets are becoming the entry point for Defi, identity, storage, computation, & social. Instead of building for each use case, Metamask is becoming a platform for apps.

- By becoming platforms, Web3 wallets are trying to onboard indirect wallet effects. Every app that joins Metamask increases the utility that users get.

History of Fintech Wallets

Paypal was one of the earliest fintech apps to achieve a major milestone by reaching one million users in 1999. Thiel attributed this success to a simple strategy-giving each new user $10 upon signing up. Paypal had a simple job to be done- send money safely over the internet. But it didn’t scale until they figured out the right distribution strategy: Ebay’s power sellers who wanted a faster means of payment than money orders. Paypal signed up over 25% of top Ebay’s power sellers and attracted a significant number of users who wanted to purchase items on eBay. New users realized that they could also use Paypal to send money to other friends who signed up or pay securely at any of the merchants supporting Paypal. The two-sided network became a critical competitive advantage, and Paypal continued to grow quicker than eBay’s own payments competitor- Billpoint. By the time eBay acquired Paypal for $1.5 Bn in 2002, the company was processing $1.5 Bn every quarter and handled 70% of eBay’s payments.

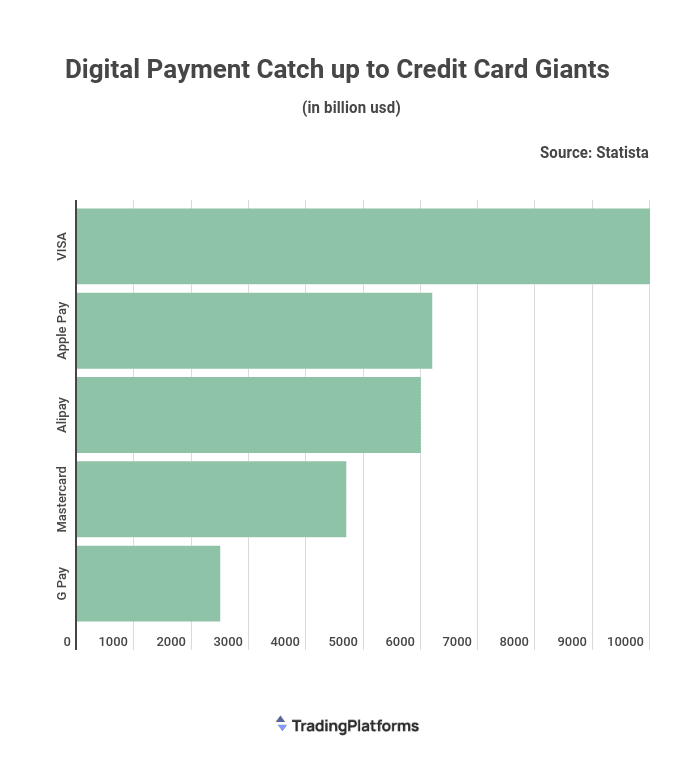

Many Web2 startups jumped onto the payments bandwagon, albeit most including Google Wallet, Chase Pay, and Square Wallet failed to grow. Successful apps like Venmo, which helps users split bills with friends, and Affirm, which allows payments to be split into installments, found specific use cases to drive growth. There are more than 300+ Fintech unicorns dominating the online payments market, closing the gap with traditional credit card giants.

A large part of the reason digital payments are catching up to Credit Cards is Apple Pay. Apple Pay already processes more payments than Mastercard and will most likely beat Visa soon. Instead of fighting with cards, Apple gave users the ability to secure their card details through tokenization and pay at any store with just a tap. By integrating themselves as the intermediary, they provide an additional layer of security and convenience for users.

While fintech apps are expanding their capabilities by integrating with banks to offer a range of financial services, such as tracking spending habits and managing savings, banks still control the power dynamic as users’ funds are ultimately stored with them.

Network Effects in Fintech

NFX is a leading researcher in startup moats and identifies four forms of defensibility - Network effects, Brand, Embedding, and Scale. They argue that network effects are the most potent form of defensibility, accounting for 70% of tech company value creation.

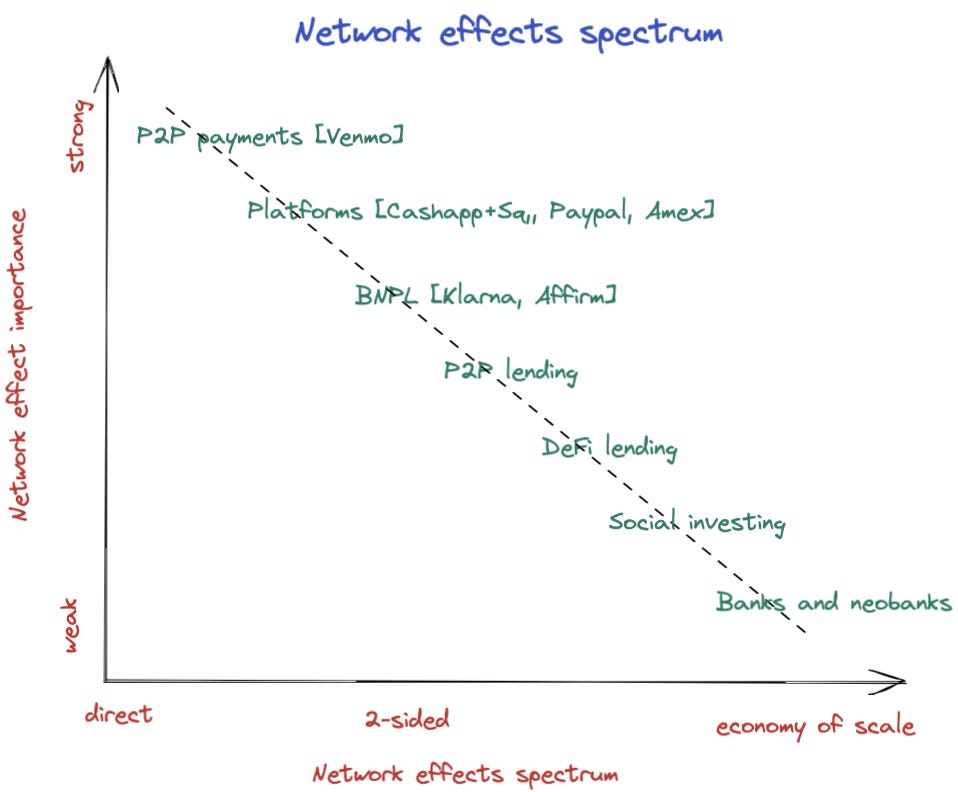

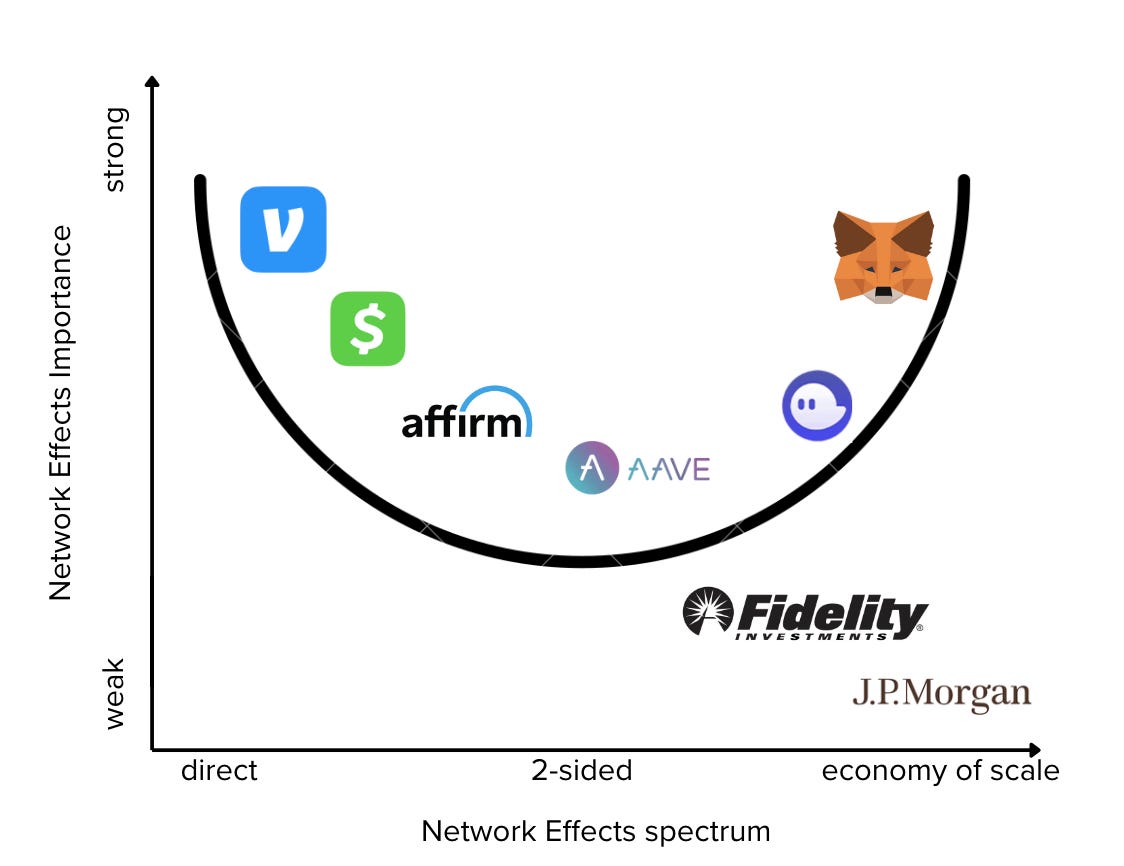

Aika, a Strategy manager at Wise wrote an excellent piece detailing the network effects of Fintech companies. She mapped fintech business models against two axes: network effects and jobs served. She observed that companies that have direct network effects can ramp up and grow very fast by having just a simple one-use-case product. On the other hand, the companies that provide deep and broad services, depend on network effects to a much lesser extent. The weaker the network effects, the more jobs the company tends to serve.

- P2P payments- Direct network effects are strong, adding one more participant increases the network of friends to send and receive money. Platforms such as Cashapp embraced this from day one and approached banking like a social media app. Even though Cash launched 2 years later than Venmo, they targeted lower-income communities that Venmo had overlooked and launched specifically in the American South region. They embedded themselves into the Black culture as Cash App’s network effect became particularly strong in the Black community. They partnered with rappers such as Lil Nas X, Travis Scott and Cardi B and announced Million dollar giveaways. If you wanted to enter the giveaway, you had to post a comment with your own #cashtag on your socials. They built a strong reputation for p2p payments before expanding their product portfolio.

- Platforms- eBay is a double-sided marketplace with indirect market effects. Adding one more seller on eBay doesn’t benefit other sellers, in fact, it increases their competition. However, having a large number of sellers increases product selection and availability making eBay more attractive to buyers. This increase in buyers brings more revenue to all merchants. BNPL platforms like Klarna and Affirm fall into this category. Affirm lets you split your purchase into installments and pay at major merchants. One more friend joining Affirm doesn’t increase the amount of utility that you as a buyer gets, but an increasing user base attracts more brands to provide Affirm option at checkout.

- P2P lending- P2P Lending faces the daunting challenge of attracting users on both sides of the marketplace also known as the ‘Cold Start Problem’. Aave the most popular Defi lending app actually started as EthLend a peer-to-peer lending market. Users were required to interact with each other using smart contracts but finding matches for lending and borrowing was not efficient because of varying parameters such as loan value and time horizon. Aave then pioneered the model of liquidity pools where users could deposit funds into a smart contract pool, and users who wanted to borrow funds could tap into this pool whenever they needed funds. By pooling assets on one end, Aave tapped into the network effect of liquidity and quickly grew from $50 Mn TVL in Jan 2020 to $1.5 Bn TVL within 12 months.

- Banks- As we move down to banks and neobanks, we can see that they perform a lot of jobs for users, and economies of scale dictate power here. Even though neobanks were perceived as an existential threat to banks, neobanks could never compete directly with banks and offer ancillary services such as account management, standing instructions, bill payments, loans. Lending/ credit/ core banking remain tightly regulated services in coordination with the central bank. Economies of scale matter here because banks require physical branches for critical services and the density of the bank’s branch presence increases convenience for users. Banks capitalize on the defensibility of Brand - users want to store their hard-earned money in a bank that has decades of credibility and trust that they will always have access to their funds.

Web3 Wallets enable Self-Banking

Web3 wallets are digital wallets that are designed to work blockchains. These wallets allow users to interact with decentralized applications (DApps) and manage their cryptocurrency assets in a secure and decentralized manner.

There are two types of web3 wallets- A custodial wallet is a type of cryptocurrency wallet where the private keys are managed and stored by a third party, such as an exchange or a web wallet provider. This means that the user does not have direct control over their funds and must trust the third party to keep their funds safe. In contrast, a non-custodial wallet is a type of cryptocurrency wallet where the user has full control over their own private keys. This means that the user has complete ownership and control over their funds, and does not have to trust a third party to keep their funds safe. When discussing web3 wallets throughout this article, we are referring specifically to non-custodial wallets, as they are the preferred way to interact with blockchains. These wallets provide users with full control over their assets and ensure that their information and assets are not vulnerable to security threats.

Web3 wallets are based on the HD Wallet setup of private key→ public key, but they require two additional important characteristics: Recoverability and Privacy. Wallets are working on ERC4337 to help users recover their keys easily and provide privacy through zk tech.

If we have to place web3 wallets along the graph of network effects vs jobs served, they would lie extremely close to banks. They are similar to banks in that, they help users store funds securely, and help them transact with various Defi applications from DEXs, savings, loans, insurance, futures, and options. Additionally, they also store NFTs, sign messages, and serve as login credentials.

They don’t derive the network effects that payment apps like Paypal have. Because these are web3 addresses, users on the receiving end don’t need to have the same wallet and just need a public address to receive funds. Web3 wallets have low lock in-users don’t need to return to the same wallet if they want to transact. They can switch their wallet by entering their seed phrase into a new wallet. This is in fact much simpler than closing a bank account and moving your funds to another bank.

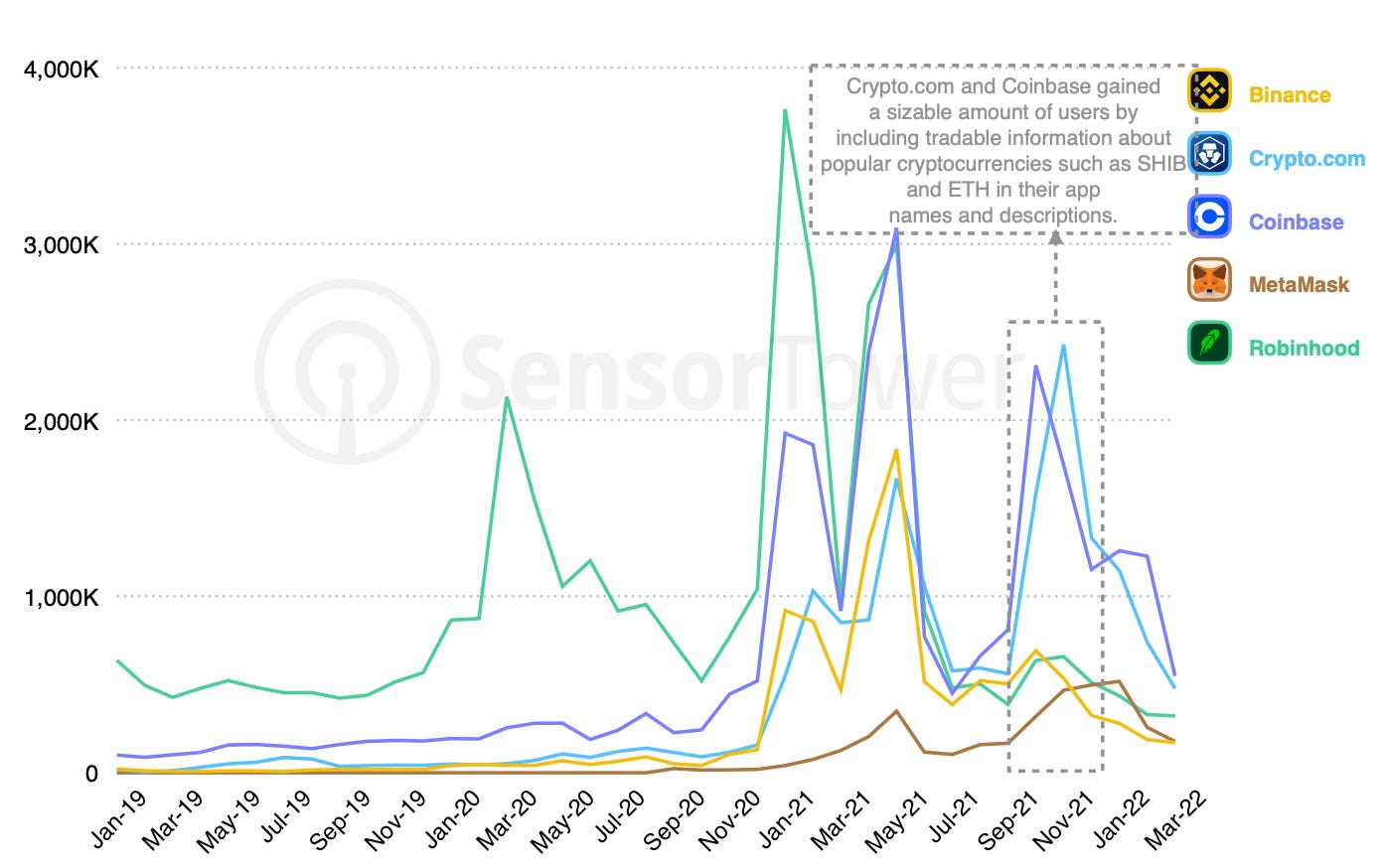

Since wallets are the primary way to interact with blockchains, they have been some of the earliest applications built out by crypto giants including Coinbase, Binance, and Consensys. While Consensys’ Metamask is almost ubiquitous on desktops, its mobile wallet needs to improve its performance and user experience. As it stands, Coinbase and Binance have taken the lead due to their superior mobile wallet offerings and the ability to on/off ramp into fiat.

Wallets as Thin Platforms

Ben Thompson argues in his thesis Thin platforms that Microsoft’s successful turnaround was based on the moving their products from thick Windows computers to thin cloud based services which could integrate data across all Microsoft users. Paraphrasing him-

Integration is exactly what Microsoft would go on to build with Teams: the beautiful thing about chat is that like any social product, it is only as useful as the number of people who are using it, which is to say it only works if it is a monopoly — everyone in the company needs to be on board, and they need to not be using anything else. That, by extension, sets up Teams to play the Windows role, but instead of monopolizing an individual PC, it monopolizes an entire company. This is where Teams thrives: if you fully commit to the Microsoft ecosystem, one app combines your contacts, conversations, phone calls, access to files, and 3rd-party applications, in a way that “just works”

How can wallets become thin platforms?

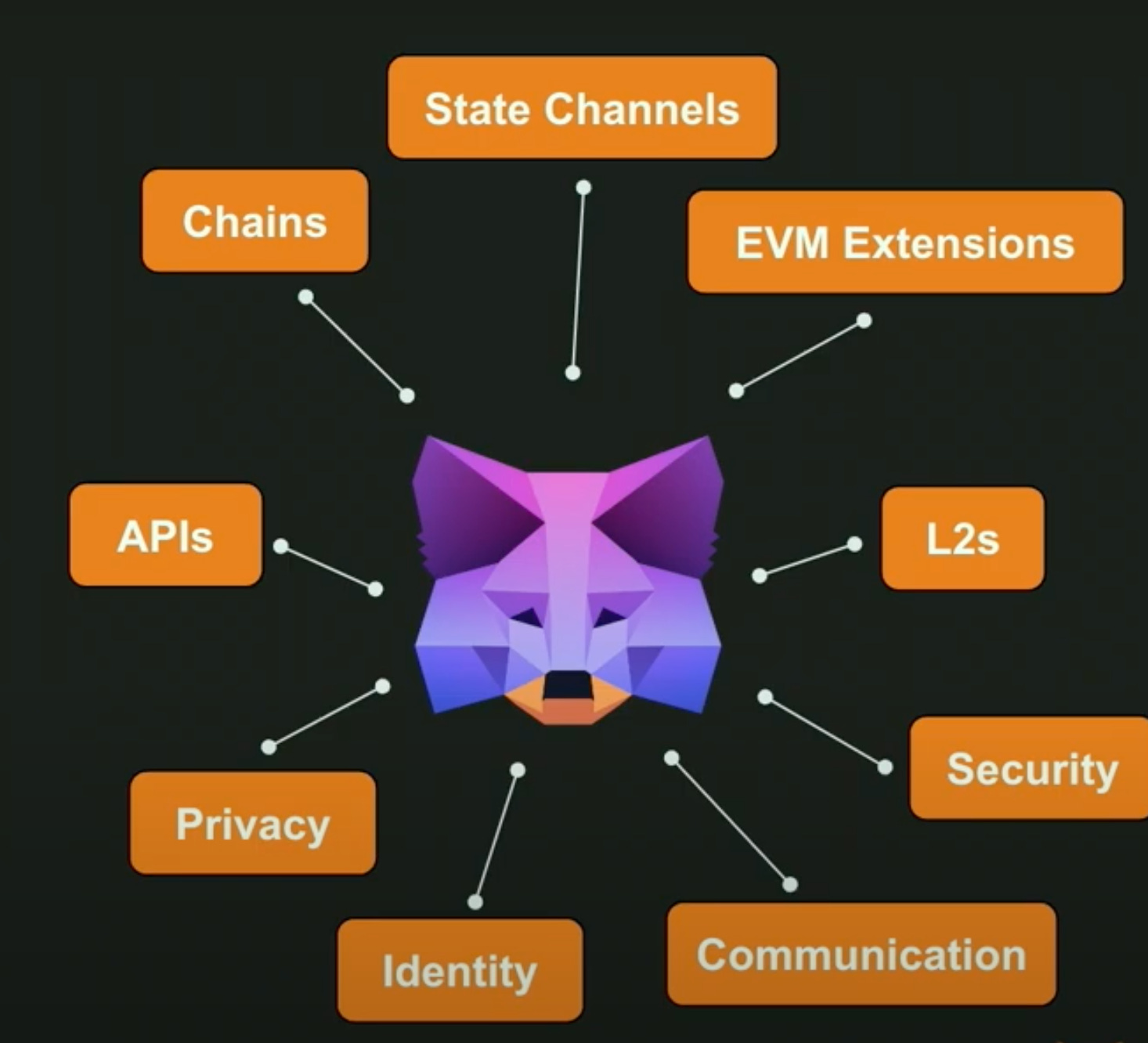

Enter Metamask Snaps. Metamask is the most popular crypto wallet with 30 Mn MAU. Metamask demoed Snaps last year as an extensible platform for permissionless innovation. Snaps are javascript programs that execute within the Metamask application and customize the wallet experience.

During the recent EthIndia event, Metamask invited devs to build on Snaps. If these submissions are anything to evaluate their potential, Metamask is onto something huge- Polysnap built a project to run arbitrary code within Metamask wallet. The project built a wrapper over Polywrap to run WASM wrappers directly inside Metamask. Cosmotic built a Cosmos wallet to support Cosmos functionality even though Metamask doesn’t support non-EVM chains. AA Snap built a developer tool to use Account Abstraction easily by setting up the basic functions. SSS built a snaps extension that semantically analyzes the transaction byte data and gives a natural language prompt using GPT-3 to the user about what the code is trying to do, not what the malicious dApp claims to do. PushSnap sends notifications directly to Metamask so that users can get reminders without downloading any additional app.

Wallets are becoming Platforms to escape competition and onboard network effects. Banks cannot succeed in doing the same because they are limited by creating a secure environment where user details can be shared with other financial . Plaid's API is one tool that enables developers to access users' banking data with third parties. But this comes at a cost of privacy and security - Plaid saves passwords as plaintext so that it can share data without user approval. With web3 wallets, the user is in complete control of the wallet and he decides which applications to interact with.

Wallets are evolving into platforms that offer more than just secure storage for user funds, providing opportunities to escape competition and harness network effects. Traditional banks face limitations in achieving the same level of success due to their primary focus on creating a secure environment and lock users into their service.

Plaid's API serves as a valuable tool for developers, allowing them to access users' banking data and facilitate interactions with third-party applications. However, this convenience comes at a cost of privacy and security concerns. Plaid stores passwords as plaintext, potentially compromising user data without explicit approval. To address these issues, Plaid is working on enhancing user control over data sharing through OAuth.

In contrast, Web3 wallets provide users with complete control over their wallets and the freedom to choose which applications they wish to engage with. This decentralized approach empowers users to determine how their data is shared and utilized, ensuring a higher level of privacy and security.

Web3 wallet protocols are building out the Lego pieces to connect multiple features that just work. Every user joining Metamask is instantly onboarded to a number of applications without them realizing it. For example - Metamask can stake a portion of your Eth into different yield farms during onboarding. Users can participate in earning passive income by staking their assets while simultaneously supporting the liquidity needs of other users, fostering a mutually beneficial environment.

Money - Pay, Save, Lend, Spend, Borrow

Chat - Discuss, Debate, Connect, DM

Access - Invites, Tickets, Events, Streams

Culture- Contribute, Curate, Earn, Create, Discover

Agreements- Votes, Proposals, Coordination, Delegation

Notifications- Alerts, Prompts, Confirmations

Metamask is becoming a Thin Platform in its own way, serving as a terminal to sync with blockchains and process user instructions. This requires them to regulate the snaps that it allows on its platform, ensuring that user funds are protected from viruses, malware, and ransomware.

Thin platforms derive network effects from the apps that are built on them. If Metamask onboards a Chat Snap, every user who installs Metamask is instantly connected to each other without the need to download a new app. In a way, Nansen added chat to make their platform more social and increase network effects.

By becoming platforms, wallets are increasing the jobs served and at the same time trying to onboard apps that drive indirect network effects to Metamask. By reducing the associated risk, wallets can become platforms where their economies of scale bring advantages to builders. Metamask's SDK supports various platforms, including iOS, Android, Unity, React, and Unreal Engine, ensuring seamless user access across all devices. Hence wallets are trying to place themselves higher on network effects vs jobs served graph forming a horseshoe.

Interestingly, Phantom is taking building network effects through embedding - integrating tightly with marketplaces and apps. Phantom allows users to list NFTs for sale on Magic Eden directly from within the wallet. Phantom also automatically takes some security minimization tradeoffs simulating transactions and identifies fraud links.

Capturing Value

By becoming platforms, wallets are trying to escape competition and retain users. Monetizing these users is tricky as the open ethos of web3 prevents lock-in and crypto-natives are wary of centralizing platforms such as Apple which charge 30% for every transaction. While we can hope that Apple is going to allow third-party marketplaces someday, Apple might still force these platforms to pay a cut for every transaction and continue extracting value.

DeFi apps are also building out wallets to increase the jobs served and become the preferred wallet for all user needs. Defi investing platforms Uniswap, Zerion and DEX aggregator 1inch launched their own wallets to service users better and solve for pain points adjacent to the main use case.

Thin platforms might make revenue in a couple of ways

- Platform Fee- Wallets can charge a take rate of the revenue that’s being processed through them. This can be a flat take rate similar to marketplaces such as Steam, Apple, and Android. However, the take rates will be much closer to what web3 marketplaces such as OpenSea are charging at 2.5% for all activity through them.

- Developer activities- Web3 wallets will serve as the entry point for all Dapps. Wallets can provide access to storage, computation, and oracles at a cheaper cost. Wallets have to run distributed nodes and ensure that their infra continuously syncs. They can provide the same infrastructure to developers and charge a premium for their consistent uptime. For example- they can deploy IPFS nodes across the globe and ensure that users are connected to the closest node.

- Embedding- Wallets can provide simplified interfaces so that users don’t need to leave their wallets for basic financial activities. Metamask Swap contributes to the majority of Metamask’s revenue with a total swap volume of $17 Bn+ and $155 Mn earnt in fees. Metamask integrates with multiple DEXs and Aggregators to swap tokens and charges 0.875% as swap fees over the native DEX fees. Even though this take rate is exorbitant compared to Uniswap’s take rate of 0.3%, new users don’t want to swap their tokens on a new platform and worry about losing their funds through a simple mistake.

Imagine a decentralized future where every website interaction is seamless. NFTs act as gateways to IPFS, with distributed infrastructure handling computation and the complete app loading up from within your wallet. This is the future Metamask is building, offering the benefit of leaving the ecosystem anytime to interact directly with apps using your private key.

Right now the Snaps integration is still under testing. With time, wallets will understand how to integrate apps into their ecosystem to give a unified user experience similar to Stripe's third-party plugins.

As wallets evolve, they are becoming operating systems to interact with blockchains and decentralized infrastructure. If you're building something cool in this space, please hit us up!